Last month’s report from the UN Intergovernmental Panel on Climate Change (IPCC) highlighted the need for urgent action on greenhouse gases, and once again put heavy-emitting sectors under the microscope. The oil & gas industry is among the most emissions-intensive, with the production and use of oil & gas accounting for more than half of global greenhouse gas emissions associated with energy consumption.

In a report out last week, environmental disclosure platform CDP analyzed 24 of the world’s largest and highest-impact publicly listed oil & gas companies on business readiness for a low-carbon transition.

European majors leading the charge

CDP’s research finds that European companies are ahead in their thinking. They account for 70 percent of the sector’s current clean energy capacity and almost all planned renewables. With less domestic pressure to diversify, US oil majors are lagging behind.

The European oil & gas majors are also thinking more long term. Many see investment in low-carbon assets as a long-term hedge against future threats to oil & gas demand. Companies need to look beyond the current cycle in order to manage climate change risks and deliver value in the long term.

Shifting assets

The research also finds that many of these companies are pivoting toward gas. In most low-carbon scenarios, gas demand remains in the mix, with the expectation it will displace more carbon-intensive coal as an industry feedstock and in electricity generation. Indeed, the share of production from gas among these companies has increased at an average rate of 1.4 percent a year since 2002 and, during this period, 17 firms have increased the proportion of gas in their portfolios.

It is also notable that five have recently divested from oil sands assets, though 10 companies still have exposure to the higher-cost, higher-carbon resource, with China National Offshore Oil Corporation – which ranks last in CDP’s league table – having the highest proportion of its proved reserves in oil sands, at 19 percent.

Under low-carbon scenarios the winning barrels will be low cost, low risk and lower carbon. These ‘advantaged’ assets should become central to company strategy. De-risking and high-grading the portfolio and managing the resource theme mix is key to attaining a low-carbon footprint.

Rising investor pressure

With climate change presenting an increasingly visible risk, it’s no surprise that oil & gas companies are coming under increasing pressure to demonstrate portfolio resilience and align with a low-carbon energy transition.

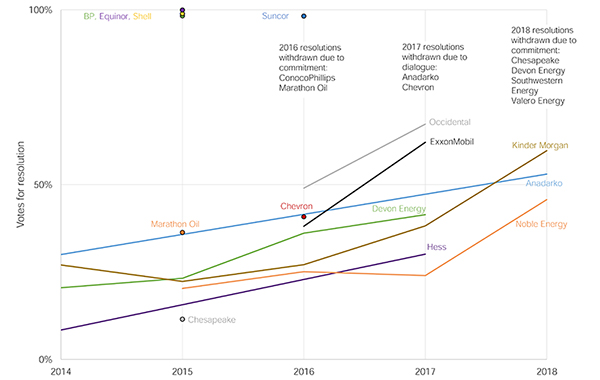

Indeed, CDP’s research finds that over the last five years, more than twice as many climate-related resolutions have been filed at oil & gas companies as in the preceding five years.

We have seen several historic milestones, most notably the votes in 2017 at ExxonMobil and Occidental, where a majority of shareholders (including the two largest fund managers, BlackRock and Vanguard) voted against management recommendations and in favor of more climate risk disclosure. This trend is seen across the industry, with resolutions calling for companies to report on portfolio resilience and 2-degree analysis gaining an increasing share of the vote.

Votes for resolutions relating to ‘reporting on 2-degree analysis and strategy’

Votes for these resolutions has grown from an average of 21 percent in 2014 to 53 percent in 2018 (a compound annual growth rate of 26 percent). Source: CDP, company reports, Ceres

But while shareholder pressure is broadly on the rise, in some cases the way investors value and analyze oil & gas companies is not driving change. Companies won’t want to transition if it is going to negatively impact their stock price, so the onus should be on investors, as well as companies, to incentivize this shift. Investors themselves need to be thinking longer term, properly pricing in these risks, and not falling back on a ‘business as usual’ investment strategy that doesn’t take climate change into consideration.

What IROs can do

IROs should encourage executives and members of the board to set clear, ambitious low-carbon targets that take account of emissions from the end-user. They should also encourage disclosure and transparency as well as the use of consistent sustainability metrics across the sector, while keeping an open dialogue with their investors about the environmental risks and opportunities they face.

Peak oil demand may come as early as the late 2020s, yet the industry’s spend as a whole on low-carbon in 2018 is expected to be just 1.3 percent of total capital expenditure. The landmark Paris Agreement drew a line in the sand: either minimize fossil fuel use or risk catastrophic consequences to our planet. And for the oil & gas industry, which is one of the most emissions-intensive, the pressure is mounting.

Luke Fletcher is senior analyst at CDP